Skeptics of outpatient joint replacement, put your seat belt on for a rapid change in perspective. Some may be surprised to learn that from 2012 to 2015 there was a 47 percent increase in elective outpatient hip and knee replacement procedures nationally, a trend that Sg2 has been predicting for years.

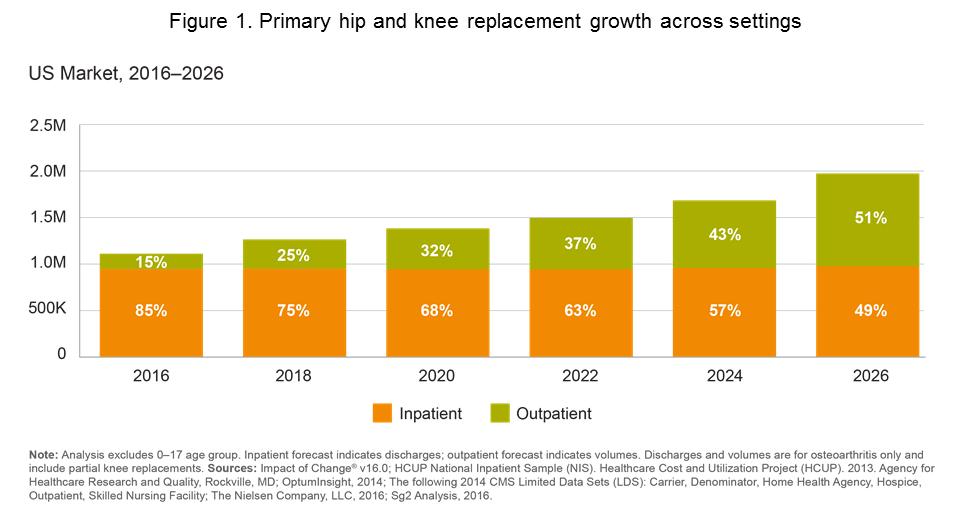

Although Sg2’s anticipated 77 percent growth in joint replacement across settings over the next decade certainly represents opportunity for orthopedic providers to target these services as growth opportunities, Sg2 also anticipates that inpatient growth will remain relatively flat at 3 percent nationally. In addition, outpatient joint replacement will continue to soar above population estimates, representing an astounding national increase of 457 percent and 633 percent in knee and hip replacement procedures, respectively.

By the end of the decade, improved anesthesia, effective pain control, and less-invasive surgical techniques, as well as advances in post-operative care management will drive the majority of elective hip and knee replacement procedures to hospital outpatient departments (HOPD) and ambulatory surgery centers (ASC). (Figure 1).

Preparing for the transition to outpatient total joint replacement

Pioneering surgeons, payers and ASC owners are fostering an increasingly favorable environment for total joint replacement in the outpatient setting. Recent CMS activity considering the removal of total knee replacement from the inpatient only (IPO) list only adds to the increasing concern of health systems to maintain orthopedic market share and margin within their communities.

“Not surprisingly, the trend toward outpatient joint replacement continues to be one of the most impactful and concerning elements to orthopedic leaders we speak with across the country,” said Kristi Crowe, associate vice president and orthopedic and spine service line lead for Sg2. “Predicting these trends in individual markets can be very challenging, as our research into recent growth has uncovered fascinating variances across local and regional markets, representing tremendous variation in both the intensity and pace of the transition.”

A robust understanding of current outpatient joint replacement activity, localized growth projections and market nuances are critical to maintaining relevance in orthopedics. According to Crowe, Sg2 provides a feasibility assessment inclusive of the following elements to determine your risk and opportunity, mitigate volume and margin loss, and develop a road map for success in joint replacement:

- Analysis of existing inpatient program to quantify organizational risk. Although the loss of substantial inpatient joint replacement revenues to a competitor hospital or ASC is an existential threat for most orthopedic programs, many are also concerned about the decreased revenues resulting from the shift of procedures to the HOPD within their current program as well.

Applying Sg2’s local forecast projections to a structured analysis of historical performance data, patient demographics, and financial considerations illuminates organizational exposure. For example, through assisting members with outpatient total joint replacement (TJR) opportunity assessments, Sg2 has found that nearly half of the total inpatient TJR patient population exhibited a length of stay of 1-2 days, a population ripe for the shift to the outpatient setting.

- Consideration of the competitive environment. Assess the level to which independent orthopedic surgeon practices might impact projected total joint volume and determine whether the local environment is conducive for orthopedic surgeon ownership of an ASC.

Orthopedic surgeons with a vested interest in an ASC can substantially steer volumes away from a traditional hospital program. It is also critical to assess the prevalence of competitor initiatives to capture the outpatient total joint market. If other providers in your community are promoting outpatient joint replacement, or merely poised to do so, determine what steps your organization might take to regain competitive advantage.

- Assessment of the payer landscape. In 2016, CMS announced that it will reconsider removal of the primary total knee replacement procedure from its IPO list. While CMS considers this action, private payers are already negotiating outpatient joint replacement carve-outs for healthier patients in many markets nationally. Ensure that clinical initiatives do not outpace development of a structure to account for changes in authorization, coding and billing activities.

Joint replacement is also a prime target for bundled payment models. Determine how merging your ambulatory and bundled payment strategies can create an attractive fixed-fee offering for commercial payers and local employers to influence referral channels.

If an assessment of the market leads you to initiate an outpatient total joint strategy, steps should be taken to promote clinical superiority and align with surgeons to develop robust patient selection criteria and support education programs for both patients and providers.

Interested in understanding your local market dynamics relative to the outpatient TJR shift? Email learnmore@sg2.com.