One of the areas of greatest concern for pharmacy practice, in terms of both cost and impact on patient care, is the increasing development of pharmaceuticals that could be classified as “specialty.” While there is no universally accepted definition of a specialty drug, most characterizations include attributes such as:

• High cost

• Limited extent of use

• Technical complexity of delivery and/or administration

• Treatment of complex and/or chronic disease states

While very important, specialty pharmaceuticals are usually thought of as only a minority of the total medication landscape, given the multitude of traditional therapies that are also used. However, based on key metrics — such as total spend and the types of new product approvals — specialty products are on the verge of representing the majority of prescribed medications.

In 2015, the FDA’s Center for Drug Evaluation and Research approved 45 novel drugs. Of those, 29 meet widely accepted characteristics of a specialty drug. In addition, 21 of the approved novel products would not just be considered specialty but are formally classified by FDA as “orphan” drugs — medications used for very rare disease states. These metrics reflect increasing investment by the pharmaceutical industry in the development of products for very limited patient populations.

According to IMS Health’s latest trend report, the 2015 total for pharmaceutical spend reached $425 billion. Specialty pharmaceuticals accounted for $151 billion, or 36 percent, of that total. In addition, of the expense associated with the growth of new branded drugs, 75 percent was attributable to specialty drugs.

To add additional validity to these statistics, pharmacy benefit management company Express Scripts placed the percent of total drug expense associated with specialty pharmaceuticals at 37.7 percent. The total expenditures on specialty drugs are expected to increase at a rate of 17 percent over the next three years. As a result, specialty pharmaceuticals are anticipated to represent 50 percent of total drug spend by 2018.

As if these statistics did not present enough concern, the outlook for the future remains exceedingly challenging by the fact that 37 percent of investigational drugs in phase II or later research are considered “specialty” products.

How should health system pharmacy practice respond?

While the challenge of specialty pharmaceuticals remains increasingly high, there are certain strategies that practitioners can implement. One key opportunity is the value brought by competition due to loss of exclusivity.

- Utilize generics and biosimilars. The recent launch of a generic imatinib should bring about price savings, particularly as more products reach the market. Also, an avenue for savings is continuing to open with the introduction of biosimilars. As evidenced by the trends identified above, failure to maximize the use of biosimilars will greatly limit any opportunities to mitigate specialty drug expense.

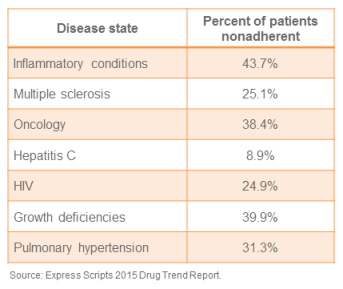

- Develop a specialty pharmacy strategy. Regardless of your practice size, focus or location, a strategy for specialty pharmaceuticals is mandatory. For some organizations, an approach will involve the development of comprehensive services. Others may choose a partnership approach with an established provider. Regardless, health systems must know exactly how their specialty pharmacy strategy enables them not only to manage cost, but also maximize patient care outcomes. As evidenced by the information from Express Scripts’ recent drug trend report, patient adherence remains a challenge even for these expensive drug categories where numerous resources are applied to maximize compliance.

Patient specialty pharmaceutical adherence for targeted diseases

Many factors contribute to nonadherence, not the least of which is drug expense. However, these statistics demonstrate how much opportunity for improved outcomes remains within the specialty pharmacy setting. Therefore, health system-based approaches have an opportunity to demonstrate leadership in driving improved compliance and better outcomes. In addition, given the penalties associated with readmissions, health systems must ensure this lack of nonadherence does not translate to additional hospital visits.

The specialty pharmacy challenge will only increase. However, tremendous opportunity for improved outcomes and more cost-effective use of therapies exist. In order to maintain sustained financial success in this area, health system pharmacy practice must demonstrate continued leadership in this area of practice.

Click here to read more blogs from this author.