There are at least two risks associated with developing strategies in a turbulent health care marketplace. The first is potential snow blindness – becoming disoriented by the appearance of so much apparent turmoil and losing focus on the horizon. The second risk is being swept up in a wave of enthusiasm for ideas that are intuitively appealing but which have relatively little probability of taking us anywhere new.

The first category of risk can cause an organization to set off in a number of different directions, searching for the right path while consuming limited resources in a series of strategic fits and starts.

The second category of risk has the potential to lurch an organization in a set direction, only to discover later that it may have been a circular path leading back to where we started.

Avoiding both categories of risk requires the focus to see through a blizzard of distractions while resisting the temptation to follow the crowd in what everyone is sure must be the way out.

Paying close attention to four economic changes will bring the horizon back into focus while providing a reliable foundation on which to anchor potential strategies:

- Retail medicine and remote/virtual care redefine health care’s front door for low acuity patient needs

- Price compression for commodity services (defined as widely available, undifferentiated services believed by consumers to be of comparable value across providers), most intensely felt in imaging and ambulatory settings, squeezes spending out of the system, leaving nowhere to hide

- Acute bundled pricing introduces “scope risk,” extending financial accountability beyond the anchor provider’s own four walls

- Longitudinal risk evolves from statistically unstable population-based spending targets and shared savings to prospective payments for chronic/complex episodes of care.

Five steps to get ready

Health systems can take a number of calculated, purposeful steps to avoid the risk of strategic snow blindness or being swept along a circular path in a wave of enthusiasm that ends not far from where we began. Here are five steps for health systems to consider.

- Prepare for a shift in consumer demand for low cost/easy access alternatives for low acuity needs.

While there may be a generational shift coming as millennials redefine consumer expectations for low acuity care, the baby boomers are also embracing alternatives to the traditional brick and mortar delivery model.

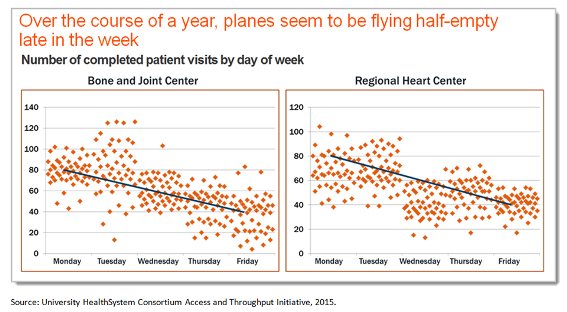

Retail clinics represent a more diffuse distribution of low acuity resources while remote/virtual encounters and technology lurk just over the horizon. Unless at least as much cost is eliminated from traditional delivery settings to offset incremental spending on retail clinics and remote/virtual care, the end result will be inflationary. - Anticipate intensification of commodity price compression. The confluence of higher deductibles and price transparency makes commodity price compression nearly impossible to avoid. Ambulatory enterprises with high fixed costs must ensure unimpeded access to avoid turning away volume in what will become an increasingly competitive battleground.

More effective capacity management – ensuring that the planes are full most of the time – will be essential to economic survival in a price-sensitive market. - Prepare for scope risk -- put PAC facility use under microscope. Acute bundled prices will mean business as usual is no longer sustainable. Discharging patients to post-acute care (PAC) facilities in order to free inpatient capacity for the next case will carry a price tag. Health systems must become more selective in which PAC facilities they use and much more careful about how often they use them. Communication and care coordination following discharge will become paramount. Managing, rather than owning the continuum of care will be the key to success.

- Accelerate the evolution of longitudinal risk from population spending targets to episodic payments.

Health systems would be wise to use their bargaining clout to move toward prospective episodic payments and away from commodity service price hikes. Higher allowed charges for commodity services will become a vulnerability as insurance deductibles continue to increase. Population spending targets are susceptible to random claims volatility and selection bias, either of which can doom a contract to failure before the game begins. Shared savings programs insulate insurers while exposing providers to significant downside risk and only questionable upside potential.

Under prospective episode payments, top performers can generate margins that are higher than those traditionally realized under fee-for-service (FFS) payment systems while avoiding incidence risk. - Meet the unmet promise of chronic/complex care coordination. Whether risk assumption comes in the form of population spending targets (e.g., accountable care organizations) or prospective episodic payments, at the core of financial success are more efficient chronic/complex episodes of care. The evidence is in – patients receiving fragmented care cost significantly more than patients who receive the majority of their physician services from a single multispecialty group.

Health systems must advance from talking about care management to delivering on the promise. The “three Cs” of a genuine group practice are essential components of success: communication, coordination, and consistency. It is not clear that a health system can achieve the efficiencies of a genuine group practice by merely aggregating horizontally or vertically; the ball is squarely in the health systems’ court to demonstrate that they can reduce variation and avoid unnecessary utilization.

The information above was excerpted from Vizient Research Institute’s 2016 Strategic Viewpoint, “Preparing for a less forgiving future: a macroeconomic point of view.” Click here to read the complete narrative. To view the narrative in a presentation format click here.

For information on other Vizient Research Institute resources, contact Erika Johnson, vice president, strategic research.