by Madeleine McDowell, MD, FAAP

Sg2 Principal and Medical Director of Quality and Strategy

For most of 2020, COVID-19 disrupted and significantly altered the infrastructure of the world’s industries, including health care delivery and services. But at what level can we expect health care to return to pre-pandemic levels? What are the long-term effects of the pandemic even as the virus generally abates while the new delta variant threatens? And what other drivers will factor into change?

The Sg2 2021 Impact of Change® Forecast lays out predictions for a rapid recovery of the health care industry, followed by ongoing shifts in where care is delivered as services move away from hospitals and other traditional settings. Here are several important trends and what to expect.

Rising acuity

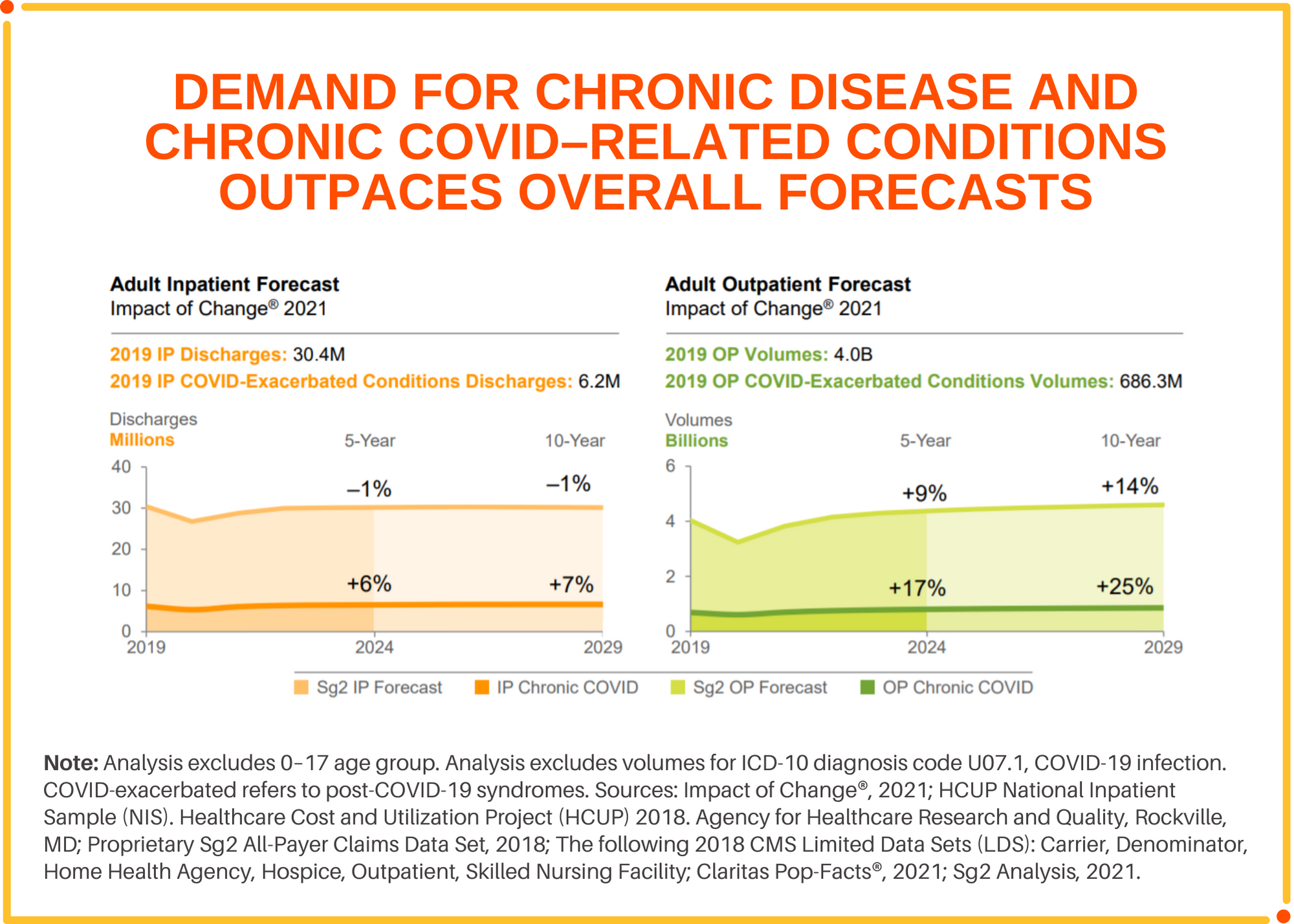

The U.S. has experienced a steady rise in chronic disease burden since 2012 which has been exacerbated by the COVID pandemic. Disruption to regular health care services during the peaks of the pandemic combined with the impact of long-COVID (or post-COVID syndrome) has resulted in a higher chronic disease burden. As a result, the pandemic has created an enduring demand for services that support long-COVID conditions that span multiple specialties, including neurology and pulmonology, behavioral health, physical medicine and rehabilitation and cardiology. The overall rise in chronic disease and co-morbidities will drive demand for new services as well as place new demands on existing services. The notable shifts in care to lower-cost settings have been in part slowed due to rising acuity.

At the same time, inpatient length of stay and acuity is projected to steadily increase over the decade. What remains in the hospital is a sicker, more complex patient driven by the aging population, rising chronic disease burden and the outpatient shift for lower acuity conditions. Nationally, despite a 1% decline in overall inpatient admissions by 2029, Sg2 projects an additional 12.5 million hospital days due to patients requiring longer inpatient stays.

A similar trend is expected in the emergency department (ED). Overall ED visit volumes are projected to decline 5% by 2029 compared to 2019 levels as lower acuity ED visits shift to alternative care sites (urgent cares, physician office, virtual). The pandemic ushered in new ways of triaging and treating non-emergent conditions outside of the ED as well as accelerated pre-existing shifts in site of care for non-emergent care. High acuity, emergent visits on the other hand are projected to grow over the decade and will make up a higher proportion of total ED volumes over time. Planning for both the hospital inpatient and ED requires taking into consideration the acuity level changes as well as the total volume changes when considering future footprint, facility design, staffing and revenue.

Site-of-care shifts

The pandemic ushered in new care models and site-of-care shifts accelerated by care redesign and policy drivers. Health care venues are shifting from inpatient to outpatient in addition to ambulatory surgery centers (ASC), provider offices and virtually.

While overall evaluation and management visits are expected to grow 14% over the decade, physician clinics are forecast to experience a 19% decline in in-person visits as patients shift to virtual care in the next 10 years. Traditional providers, insurers, as well as new market entrants are offering a host of virtual services that are more convenient and less costly. Ultimately, patients will be seen in the office for more complex issues that require comprehensive evaluations, diagnostics and ancillary services. Non-visit services in physician clinics, such as office-based diagnostics, lab testing and imaging are projected to grow 18% by 2029.

Shifts in specific surgeries from the inpatient to the hospital outpatient department and ambulatory surgery centers (ASCs) are expected because of clinical innovation, payer pressures and physician preferences. Contributing to this trend is increasing private equity investment in ASCs, particularly in markets ripe for surgical volume shifts. Hospitals should anticipate not only surgeries shifting sites within their health system but also moving away from their system altogether to private equity-backed physician-owned ASCs. Hospitals that do not have alignment with their surgeons can expect to see greater impact from these shifts, losing not only surgical volumes but other service volumes associated with the surgical episode including imaging, diagnostics and rehab visits.

In addition, health systems are making major investments in their ability to provide care to patients from the comfort of their own homes. These programs enable patients who would traditionally be hospitalized to be managed in the home with remote monitoring and virtual connections to the hospital team and with in-person visits by a nurse or doctor.

Part of the growth in site-of-care change will be attributable to a reimagining of senior care that moves patients out of skilled nursing facilities due to clinical and digital advances that enable post-discharge care to be done in the comfort of the home. Despite an aging population, skilled nursing facility stays are projected to decline 5% by 2029 as remote monitoring and aging at home models are increasingly adopted.

What COVID leaves behind

In its wake, the pandemic was responsible for unprecedented human loss and long-term health implications we are only beginning to understand. The disruption it had on health care delivery allowed for rapid adoption of new care models, some of which will have enduring impacts on how care is delivered. Rising acuity, virtual and digital innovations and the shift to lower-cost settings will contribute to the ongoing restructuring of the current system of care. Understanding future clinical demand and how it is changing is critical for planning for future resources, workforce, facility and program development.

About the author

Madeleine McDowell leverages a decade of clinical experience in leading the development and application of Sg2’s data analytic tools and providing clinical insight for all Sg2 research. As medical director, she provides thought leadership in quality in collaboration with experts across the Vizient and Sg2 organizations and partners with member health systems as a strategic advisor and health care industry expert in market strategy, quality and analytics. Her involvement with the annual updates of Sg2’s Impact of Change® forecasts and CARE Grouper ensures rigorous clinical oversight is applied. In addition, she oversees the development of new data analytic methodologies and integration with Vizient analytics.