In health care economics, hospitals have long held the top spot. While that is unlikely to change from a cost perspective, trends in patient utilization suggest their economic viability may soon hinge on how well they manage care delivered outside their four walls.

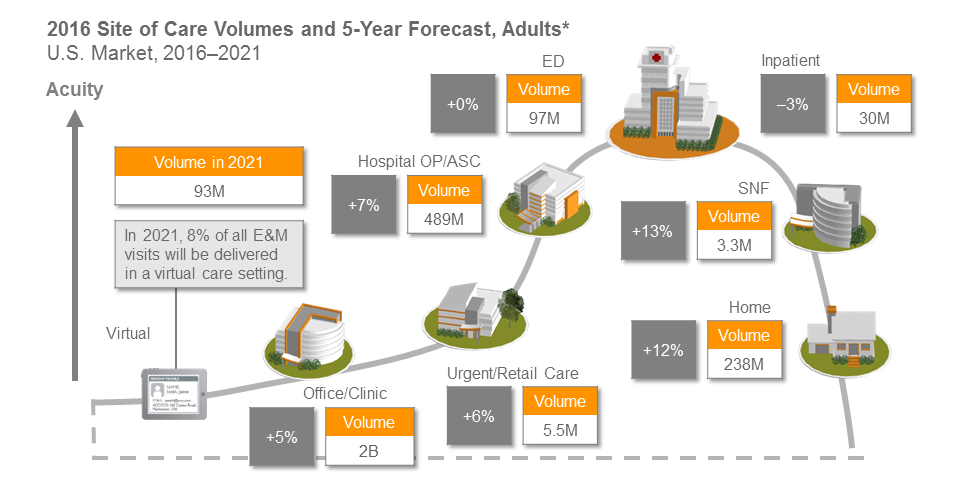

Sg2’s Impact of Change forecast, which analyzes year-over-year demand shifts by site of care, projects that patient care in non-acute facilities is expected to grow by 8 percent through 2021 and inpatient care is projected to decline by 3 percent over the same time period.

The study found that the migration of patient care will most dramatically impact skilled nursing facilities, home/hospice care and hospital outpatient/ambulatory surgery centers. Driving these increases in patient volume to facilities outside of the hospital are changes in reimbursements, alternative payment models, population health management and technology.

These trends pose challenges for hospital supply chain leaders already struggling to manage supply spend at the non-acute facilities within their health system. “What we regularly hear is they have a hard time quantifying the amount of spend by their non-acute facilities. Adding to that is they don’t have the visibility or data to understand the purchasing habits, contract compliance, vendor utilization and pricing at those facilities,” said Richard Peters, associate vice president, non-acute, for Vizient.

To help hospital supply chain leaders prepare for the expected shift in patient volumes in a manner that enables cost savings for the organization as a whole, Peters suggests asking these questions to assess your organization’s readiness for this shift:

1. Do you have a specific strategy for non-acute care such as acquisitions or joint ventures?

"In response to health care reform, most of the health systems served by Vizient are pursuing targeted strategies that will enable them to offer a full suite of health care services across the continuum of care,” said Peters. Each member and market is different but here are a few ways these strategies are appearing:

- Buying primary care physicians to ensure the health system captures patients at the beginning of the care continuum

- Partnering with home-care or long-term care providers to ensure patients follow their discharge orders to minimize readmissions due to complications from their inpatient stay

- Building a joint venture surgery center with leading specialty physicians to provide quality care in the ambulatory surgery center setting

2. Do you have a supply chain strategy to support your non-acute strategy?

Supply costs and savings opportunities naturally extend to facilities outside the four walls of the hospital and are a good source of value to a health system. However, if not managed correctly they can also be a sore spot. “A specific non-acute strategy, built with your non-acute providers in mind, would help address the different services they need, specific product categories they are passionate about and also help you understand what they might be expecting from their relationship with the health system,” said Peters.

3. Do you have a non-acute supply chain savings target?

If you do not have a target, it is likely that your providers and their supply chain managers will keep making the same buying decisions, limiting any progress. Oftentimes, the best results are seen when the hospital supply chain leader collaborates with their non-acute providers to establish a supply savings target. This demonstrates that the non-acute providers are an important part of your organization and gives them a sense of ownership for the goal. If an overall savings target is not the right metric for your organization, start with a product category standardization goal to drive some efficiencies and product consistency.

4. Do you know how much your organization spends on non-acute supply chain products and/or services?

When asked this question, providers either have an easy answer or it quickly becomes a point of discussion, ultimately demonstrating a need to improve transparency and the availability of data. Health system supply chain leaders without good visibility should start the process of understanding non-acute spend by reviewing distribution channels, AP files and if applicable, leveraging their MMIS data.

5. Do you have a designated leader in your organization driving change or improvements in the non-acute supply chain?

“I cannot emphasize enough the importance of having someone who is focused on making improvements as a large part of their daily jobs. Too often we have seen busy supply chain professionals ‘inherit’ non-acute when their bandwidth is already at capacity just keeping up with the demands of the hospital,” said Peters. “Without a non-acute supply chain strategy owner, it won’t have the focus necessary to be successful.”

The reality for hospital supply chain leaders at health systems with affiliated practices and facilities is that patient migration essentially moves the goal posts for your success. Addressing the questions above can help you begin to frame a non-acute supply chain strategy that will position your organization to deliver the highest level of cost-effective care in every setting.

Click here to read how Freeman Health System in Joplin, Missouri achieved supply chain savings for their growing non-acute care business.

For supply chain leaders looking for non-acute solutions, Vizient has a dedicated staff of non-acute specialists who can help take your organization from strategy to opportunity identification to tactical implementation. For more information, please visit www.vizientinc.com/nonacute or email us at nonacute@vizientinc.com.

*Analysis excludes 0–17 age group. Other sites not listed, including nonhospital locations such as OP rehab facilities, psychiatric centers, hospice centers, Federally Qualified Health Centers and assisted living facilities, represent 8% growth from 2016-2021 and a baseline volume of 206 million.. ASC = ambulatory surgery center; CARE = Clinical Alignment and Resource Effectiveness; E&M = evaluation and management; SNF = skilled nursing facility. Sources: Impact of Change® v16.0; HCUP National Inpatient Sample (NIS). Healthcare Cost and Utilization Project (HCUP). 2013. Agency for Healthcare Research and Quality, Rockville, MD; OptumInsight, 2014; The following 2014 CMS Limited Data Sets (LDS): Carrier, Denominator, Home Health Agency, Hospice, Outpatient, Skilled Nursing Facility; The Nielsen Company, LLC, 2016; Sg2 Analysis, 2016.